PART I

ITEM 1. Business

Company Overview

We are an end-to-end, full-service programmatic advertising platform primarily focused on providing advertising technology, data-driven campaign optimization and other solutions to underserved and less efficient markets on both the buy- and sell-side of the digital advertising ecosystem. Direct Digital Holdings, Inc., incorporated as a Delaware corporation on August 23, 2021, is the holding company for DDH LLC, the business formed by our founders in 2018 through the acquisitions of Huddled Masses and Colossus Media. Colossus Media operates our proprietary sell-side programmatic platform operating under the trademarked banner of Colossus SSP™. Huddled Masses is the platform for the buy-side of our business. In 2020 we acquired Orange142 to further bolster our overall programmatic buy-side advertising platform and enhance our offerings across multiple industry verticals such as travel, healthcare, education, financial services and consumer products with particular emphasis on small and mid-sized businesses transitioning into digital with growing digital media budgets. In February 2022, we completed our initial public offering and certain organizational transactions which resulted in our current structure.

In the digital advertising space, buyers, particularly small and mid-sized businesses, can potentially achieve significantly higher return on investment (“ROI”) on their advertising spend compared to traditional media advertising by leveraging data-driven over-the-top/connected TV (“OTT/CTV”), video and display, in-app, native and audio advertisements that are delivered both at scale and on a highly targeted basis.

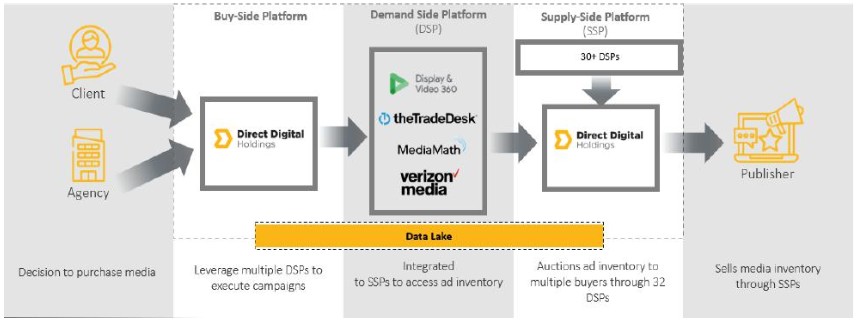

Programmatic Marketplace Transaction

The Buy Side

On the buy side of the digital supply chain, digital advertising is the practice of delivering promotional content to users through various online and digital channels and leverages multiple channels, platforms such as social media, email, search engines, mobile applications and websites to display advertisements and messages to audiences. Traditional (non-digital) advertising follows the “spray and pray” approach to reach out to the public, but the ROI is mostly unpredictable. On the other hand, digital advertising is heavily data-driven and can give real-time details of advertising campaigns and outcomes. The availability of user data and rich targeting capabilities makes digital advertising an effective and important tool for businesses to connect with their audiences.

We have aligned our business strategy to capitalize on significant growth opportunities due to fundamental market shifts and industry inefficiencies. Several trends, happening in parallel, are revolutionizing the way that advertising is

4